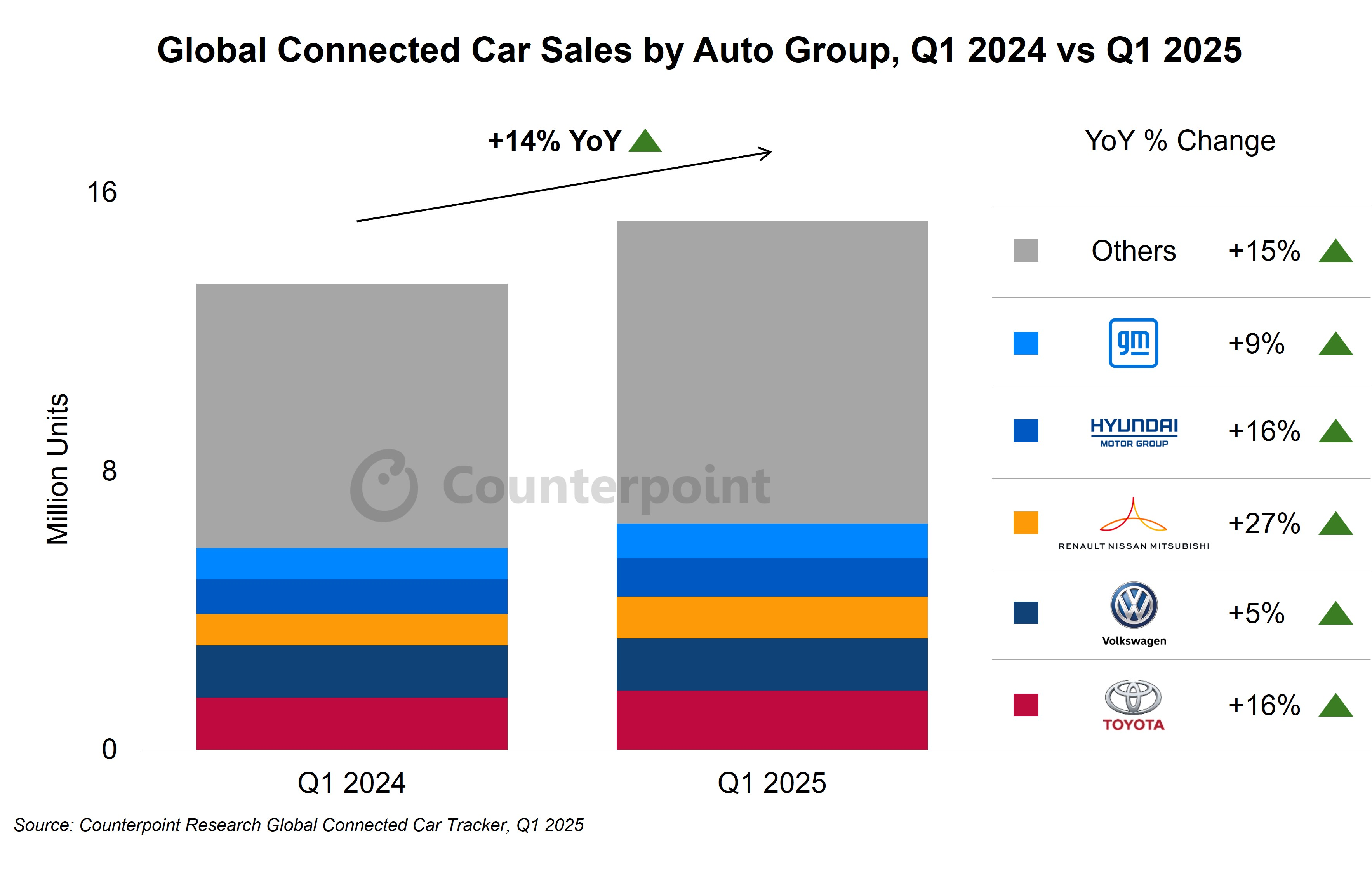

According to the latest data from market research firm Counterpoint Research, global connected car sales in the first quarter of 2025 increased by 14% year-on-year, with 76% of new cars equipped with embedded networking functions, marking the comprehensive entry of the automotive industry into the intelligent competition stage. In this new battlefield centered on the "Internet of Vehicles", Chinese car companies are rewriting the pattern with an absolute advantage of 5G technology penetration rate three times higher than the world's. BYD has become the global growth king with a year-on-year growth rate of 55%, while Toyota, although temporarily leading with an 11% share, is rapidly being eroded by the Chinese army.

Market pattern: from "European and American dominance" to "East West divide"

1.BYD's "dual cycle" growth engine

●Domestic foundation: Covering the mainstream market of 100000 to 300000 yuan through the DiLink system, the penetration rate of networking functions reaches 92%.

●Overseas breakthrough: Launched the "5G+high-precision map" package in Southeast Asia and Europe, with a 230% increase in order volume compared to the previous period.

●Technical dimensionality reduction: Compressing the cost of in car 5G modules to $85, which is 40% lower than the industry average price.

2. Toyota's "defensive" layout

● High end market: Lexus comes standard with 5G+V2X, but the starting price of 350000 yuan excludes the mass market.

●Ecological weakness: The number of Toyota's in car system apps is only 63, which is less than one-third of BYD DiLink.

5G car explosion: Why can China monopolize 70% of the market?

1. Release of infrastructure dividends

● Base station density: China has 19.8 5G base stations per 10000 people, which is 3.2 times that of the United States.

●Policy leverage: 11 cities are piloting "vehicle road cloud integration", requiring new L3 level vehicle models to be compatible with 5G.

2. Formation of technological generation gap

●Localization advantage: Huawei and ZTE provide vertical solutions from modules to the cloud, with response times shortened to 2 weeks.

●Cost black hole: Non Chinese car companies' 5G models have an average premium of 23000 yuan, while BYD has controlled the premium within 8000 yuan through self-developed chips.

Competitive Transformation: 5G From 'Chinese Specialty' to 'Global Standard'

1.Horn of counterattack for foreign brands

●Volkswagen ID.7: Launching the "5G+ChatGPT" package in Europe, with a monthly subscription fee of 49 euros.

●Tesla HW4.5: Achieving "no base station networking" through satellite communication, but with a latency of up to 800ms.

2.BYD's' Next Battle '

●Technology bet: Mass produce 3nm process automotive chips by the end of 2025, with computing power reaching 400TOPS.

●Ecological Barrier: Jointly build an "Intelligent Automotive Application Store" with Tencent and Alibaba, reducing the sharing ratio to 15%.

Industry Insights: The Connected Car War Enters the 'Second Half'

1. End of hardware profit model: The price of in car 5G modules has dropped by an average of 28% annually, and car companies need to profit from software services.

2. Data sovereignty battle: Chinese car companies generate an average of 1.2PB of driving data per day, which is five times that of foreign brands.

3. Security standard upgrade: The Ministry of Industry and Information Technology requires that new cars must pass the "Compulsory Certification for Automotive Network Security" by 2025.